Given the pace at which the world aims to decarbonise by transitioning away from fossil fuels towards a low carbon economy, demand for the commodities needed to achieve a net-zero future has surged, raising questions around supply.

Vanadium is one of the critical commodities required in the clean energy transition. As the 22 nd most abundant element in the earth’s crust, vanadium is more abundant than some of the other critical future metals including copper, nickel, cobalt, lithium, and chrome.

With 22 million metric tonnes (mt) of known global reserves of vanadium, there is enough vanadium in the ground to meet current market demands for more than 150 years, with several potential high-grade undeveloped vanadium projects identified globally, and several untapped secondary sources of vanadium capable of being exploited.

Vanitec, the not-for-profit international global member organisation whose objective it is to promote the use of vanadium-bearing materials, says that while vanadium is mainly used within the steel industry, vanadium is increasingly being recognised for its use in vanadium redox flow batteries (VRFBs). These long duration batteries can store large amounts of electrical energy produced by solar and wind power generators daily to drive the deep decarbonization of electric power systems.

Demand drivers of vanadium

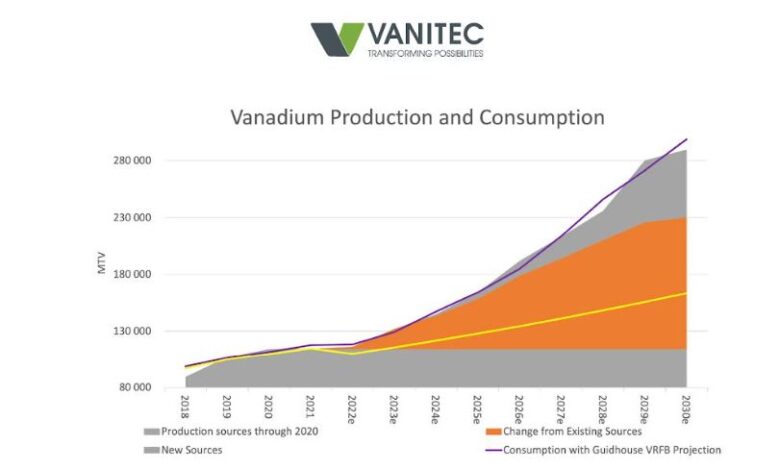

According to data published earlier this year by market intelligence and advisory firm, Guidehouse Insights, global annual deployments of VRFBs are expected to reach approximately 32.8 GWh per year by 2031. Based on this projection by Guidehouse, the total amount of vanadium needed to meet this level of VRFB deployment would equate to 130,000 mt of new vanadium per year by 2030, according to Vanitec calculations.

VRFBs are not the only demand driver of vanadium consumption. About 90% of vanadium demand comes from the steel industry, with around 6-7% demand from the chemical industry and around 2-3% demand from the titanium alloy industry.

“When adding the potential forecast vanadium demand from energy storage to the current data on total vanadium consumption, the forecast shows that total vanadium demand could increase to close to 300,000 mt by 2030 from the current 115,000 mt of annual vanadium consumption,” Terry Perles, Director of US Vanadium – a Vanitec member company – said during the organisation’s 11 th Energy Storage Committee Webinar in September.

“This equates to a doubling of demand for vanadium over the next eight years, driven primarily by the growth in VRFB demand” Perles highlighted.

While the average growth rate in global vanadium production volume has increased by about 7% a year over the past two decades, vanadium production volume will need to grow by a little over 10% each year for most of the balance of the decade to meet the future vanadium demand that Guidehouse forecast.

Current and future vanadium production

About 128,000 mt per year of vanadium is produced globally, with significant potential to unlock further vanadium production capacity in the coming years through capacity expansions of current vanadium producers and the recommissioning of idled production plants. According to Perles, doing so could unlock just over 100,000 mt of additional vanadium production. The capacity expansions have the highest probability of realisation with the fastest route to production.

In addition to capacity expansions, Perles estimates that about 70,000 mt of new sources of production through greenfield project development would be required to reach the estimated 300,000 mt of future vanadium demand. Most of the recent greenfield projects announced for development are of a co-production or multi-commodity nature.

China is expected to continue to remain a major source of vanadium supply in future, followed by Australia, which is expected to emerge as a major supplier in the coming years through the establishment of new vanadium projects in the country. Somewhat smaller, but still important, new vanadium supply is expected to emerge from the Middle East towards the middle of the decade, said Perles, primarily in the form of secondary vanadium materials recovered from petroleum residues from the oil industry.

Raw material sources of vanadium

There are three major sources of raw materials that support vanadium production globally. The most important source is co-product steel slag, which is a vanadium bearing slag containing 14-24% vanadium trioxide content. This slag is produced as a co-product during steel making from the processing of vanadium-bearing magnetite ores. This source of vanadium currently supplies about 70% of the world’s vanadium needs.

Vanadium is also extracted from primary sources, which are mining operations that typically extract vanadium from vanadium-titanium-bearing magnetite ore bodies in countries including South Africa, Brazil, and China. Moreover, there is potential to extract vanadium from stone-coal mining operations in China, and from a large multi-element mining project potentially currently in development in Kazakhstan in future.

Lastly, there are secondary material sources of vanadium, in which vanadium (and other trace elements such as nickel) is recovered from the petroleum industry, including petroleum residues and the recycling of spent catalysts used in crude oil refining.

A new standard reducing the allowable sulphur content in bunker fuel for ships was imposed in 2021. As a result, we will see significant increases in vanadium available for recovery from spent heavy oil residue upgrading catalyst in the next few years. Facilities are under development now to process these spent catalysts and contribute to the vanadium supply base.

“Because it takes much less time to develop a secondary vanadium material production facility to recover vanadium than it is to develop a new vanadium mine, we expect to see significant increases in secondary sources of vanadium in the near term, with new primary sources of vanadium coming online in the longer term, said Perles.