Seifsa load shedding impact assessment on the metals and engineering sector

The energy crisis that is gripping South Africa presents the most significant risk and binding constraint to the economic prospects of the country.

The crisis not only has implications on the immediate survival of companies but also on the long-term implications regarding the investment prospects of the country. The crisis has been particularly damaging on the metals and engineering sector, a sector which is the backbone of industrialisation and to which electricity, particularly baseload electricity, is fundamental to its survival.

SEIFSA represents 18 Employer Associations, who collectively represent in excess of 1 300 companies and employ in excess of 170 000 employees in the metals and engineering (M&E) sector. The M&E sector constitutes 26.5% of the manufacturing sector, based on output, and 2.6% the country’s gross domestic product (GDP) on a value-add basis. As at December 2022 the sector employed 374 496 (of which 217 618 are factory workers) who are employed in approximately 10 00 companies.

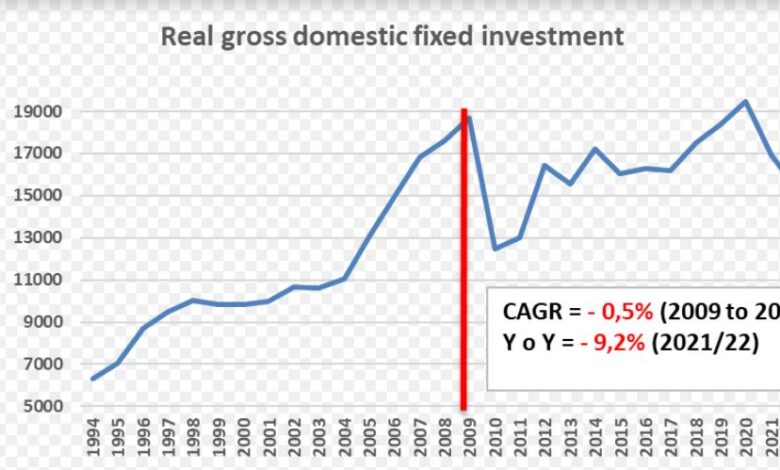

It is important to highlight, in brief, the historic context in which this survey is conducted. The M&E sector has been in a structural recession since the global financial crisis of 2008/9, with production recording a 1.2% contraction on a compound annual basis over this 15-year period. Given the less supportive global economic environment and the impact of domestic rigidities, chiefly the energy crisis, production in the sector is expected to contract further by 2.2% in 2023. Unfortunately, employment in the sector has also mirrored the production trends contracting at -1.1% (CAGR) and contributing to the country’s unemployment crisis. These trends are contained in the graph below. The Covid-19 induced lockdowns presented a major economic shock to the sector and although the production levels recovered (still 1% below pre-covid levels), employment trends have not (4.6% below pre-covid levels). Increasingly the sector has observed a weakening relationship between production and employment, meaning improving production outcomes are no longer a necessary condition for employment creation.

The intensifying electricity crisis now presents the most prevalent economic risk to the sector:

It is in this context that SEIFSA undertook to survey its affiliated membership and developed this load-shedding impact assessment. This survey measures the impact of the energy crisis over a 12-month period (February 2022 to February 2023) across four main parameters, namely:

- Employment;

- Production;

- Investment;

- An analysis of the alternative energy investments made by the sector; and

- Impact to Input costs.

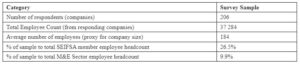

The survey garnered a positive response, with 206 companies responding. The survey parameters are included below:

The employee headcount is the pivot variable for the purposes of consolidating the statistics, particularly the weighted outcomes. The companies that responded to the survey vary in head count from 2 employees to 2600 employees.

The straight average headcount across the sample is 184 employees yielding a good mix between large, medium and small companies. The definition of small to medium companies in the sector, based on headcount, is 50 employees or less. These companies represent 41.3% of the sample. The histogram below indicates the distribution of the company sizes relative to employment:

The consolidated results of the survey are contained in the table on the next page.

It is necessary to bear in mind that these results are from a sample representing 10% of the sector (measured on an employment metric).

Theoretically, the outcomes, particularly the absolute numbers, could be multiplied by 10 to get the full impact on the sector.

Consolidated results of the survey:

Employment:

- The employment losses, mostly attributable to companies responding to the energy crisis over the reference period, indicate some very concerning trends.

- A quarter of companies indicated that they have had to reduce head count in response to the electricity crisis, by as much as a quarter of their employment, equating to 9 432 people.

- A third of the sample indicated that they are working short-time due to the electricity crisis.

- An even more concerning outcome is the fact that half (16.9%) of those companies that are implementing short time have already reduced head count.

- We assign the status of “vulnerable” to these companies, while the other half (17.3%) have not reduced head count, however, short time is a good leading indicator to track for potential future job losses.

Production:

- The respondents to the survey indicated production declines as much as 34.2% (weighted) as a result of the electricity crisis.

- Based on the model in the table below, SEIFSA has calculated that production in the sector is estimated to contract by 2.2% in 2023.

- However, factoring in the results from this survey, the forecast for the 2023 year deteriorates to – 5.3% for the 2023 year.

Investment:

- The long-term implications of this energy crisis to the future prospects of the sector are devastating.

- Over the last 15 years, net-investment into the sector has been on the decline, which has led to the value of fixed capital stock deteriorating at -0.3% (CAGR), threatening the competitiveness of the sector.

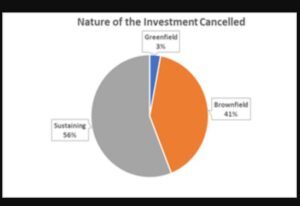

- It is therefore concerning that 42.6% of companies have indicated that they have cancelled investment and/or expansion plans owing to the uncertainty presented by the electricity crisis.

- The value of these investments amounts to R2.64 billion with the potential of creating 1 620 new jobs. The split of the nature of investment is included below.

An analysis of the alternative energy investments made by the sector:

- 2% of companies indicated that they have had to install alternative electricity sources in the last 12 months to counter the pressing challenge presented by the electricity crisis.

- The combined value of this investment is R985 million. This number if considerable when considering that it accounts for 37% of the value of investments cancelled. This again highlights the point that SEIFSA has repeatedly stressed that companies are sacrificing scarce long-term capital to fulfil an immediate survival, presenting long-term adverse implications regarding the sustainability of the sector.

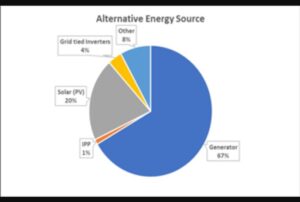

- The breakdown of the alternative technology source invested into is contained in the pie chart below. It is not surprising that given the relatively intense electricity consumption nature of the sector, the most practical alternative energy sources are generators representing 67%.

- Solar accounts for 20% of the investment made. It should however be borne in mind that this survey was done prior to the announcement of the 125% tax incentive afforded to companies in the February 2023 National Budget. This incentive should result in an increase in the up-take of solar an alternative source, however, the electricity consumption profile of the sector remains a limitation to solar being a full-scale option.

- On aggregate the companies have a generator installed capacity of 116MW, while that of solar is 36.2%.

- The respondents have registered very limited ability to feed-in any excess electricity generated from their solar installations, largely because of the fact that the solar installations have been put in as a marginal hedge or top-up to their baseload needs. This picture may well change given the 125% tax incentive, although to a limited degree, because the sectors electricity consumption pattern is the main determinant for the technology deployed.

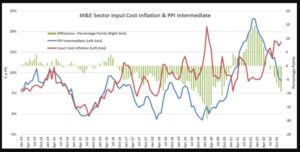

Input Costs:

- On a weighted average basis, companies have indicated increases to monthly operating costs to the extent of 24.9% from the extensive use of generators.

- This does not bode well for a sector whose input costs are running at 17.6% (y o y – February 2023).

- Factoring in the results of the survey to the input cost model results in input costs increasing by 1.7 percentage points to 19.3% for the sector.

- The less supportive demand environment means that these companies cannot easily pass on these costs, thereby resulting in considerable margin squeeze and ultimately long-term sustainability.

We would like to thank the SEIFSA affiliated membership who have taken the time to complete this load shedding impact assessment survey. The results of the survey are extremely valuable in providing tangible and quantifiable results which are necessary in various engagements SEIFSA will be having with key stakeholders responsible for resolving South Africa’s gripping electricity crisis.